Launching a company in Saudi Arabia is an exciting milestone.

The Commercial Registration (CR) is approved, the entity is officially active, and operations are ready to begin. For many founders, that feels like the finish line.

In reality, it is the starting point.

The moment your Saudi company becomes active, the clock starts ticking on finance governance, tax compliance, audit readiness, and operational controls. And this is where many new businesses make their first major mistake.

They treat compliance like a “future finance problem.”

Unfortunately, by the time companies decide to organize their books properly, the damage is often already done:

- Missing invoices

- Unclear founder transactions

- Poor audit trails

- Delayed ZATCA registrations

- Unreconciled bank accounts

- Informal approvals with no documentation

Cleaning up six months of financial disorder is always more expensive than building proper controls from day one.

This guide provides a practical framework for new companies in Saudi Arabia to establish finance governance immediately after incorporation. Whether you are a startup founder, finance manager, foreign investor, or scaling SME, these steps will help you build a clean, audit-ready operation from the beginning.

What Is a Day-One Compliance Plan for a New KSA Company?

A day-one compliance plan in Saudi Arabia is a structured framework implemented immediately after incorporation to ensure audit readiness and regulatory compliance. It includes setting up a chart of accounts, defining approval workflows, capturing audit evidence for early expenses, and registering with key authorities such as ZATCA, GOSI, and MHRSD before operations fully begin.

Why Finance Governance Can’t Wait

One of the biggest misconceptions among new businesses is believing compliance only matters once revenue starts flowing.

That mindset creates operational risk almost immediately.

In Saudi Arabia, compliance is not limited to tax filings. It also includes:

- Financial recordkeeping

- Internal approvals

- Payroll controls

- Audit evidence

- Government registrations

- Contract documentation

- Bank reconciliation processes

- VAT and Zakat readiness

Even small startups are expected to maintain proper documentation standards.

Auditors, investors, regulators, and banks will not overlook missing records simply because the company was “new.”

The Myth of “We’re Too Small for Controls”

Many founders assume governance processes are only necessary for large enterprises.

But even a five-person startup can face serious operational problems if:

- Expenses are undocumented

- Payments are made without approvals

- Personal and business funds are mixed

- Employee records are incomplete

- Tax registrations are delayed

Strong controls early on actually make businesses move faster later.

When finance systems are structured from the beginning, companies avoid painful cleanup projects during:

- Investor due diligence

- Tax reviews

- External audits

- Bank compliance checks

- Acquisition discussions

Building an Audit Evidence Mindset

The goal of early finance governance is simple:

Every transaction should have a traceable story.

An auditor should be able to follow:

- Who approved the transaction

- Why the payment was made

- The supporting invoice or contract

- The bank transaction

- The accounting entry

This applies even to the earliest business expenses.

For example:

If a founder pays for company software subscriptions personally before the corporate bank account is active, there should still be:

- The invoice

- Proof of payment

- A reimbursement approval

- Proper accounting treatment

Without these records, future audits become difficult very quickly.

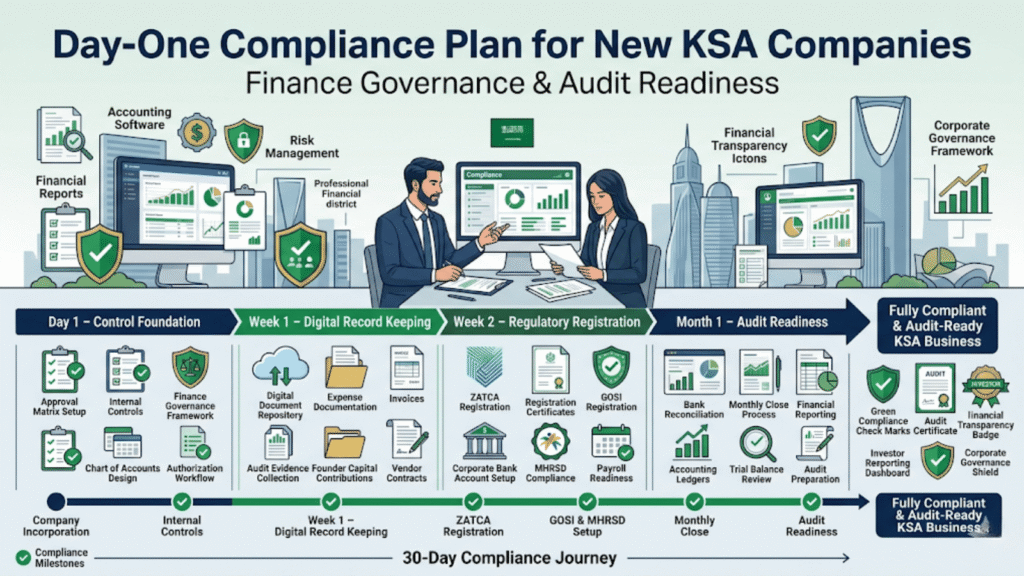

The First 30 Days: A Practical Compliance Roadmap

Day 1: Establish the Control Matrix

The first day after incorporation should focus on financial structure and authority controls.

Do not wait until the company grows.

Define Approval Responsibilities

Clarify:

- Who can approve vendor onboarding

- Who authorizes payments

- Who reviews contracts

- Who posts accounting entries

- Who has banking access

Even in founder-led companies, approval responsibilities should be documented formally.

This protects both the company and the founders themselves.

Set Up the Chart of Accounts

A proper chart of accounts creates the foundation for:

- Financial reporting

- VAT treatment

- Audit readiness

- Budget tracking

- Investor reporting

Do not rely on random spreadsheets or inconsistent account names.

Structure matters from the beginning.

For example:

Instead of recording everything under “Miscellaneous Expenses,” separate categories clearly:

- Professional Fees

- Software Subscriptions

- Government Fees

- Employee Costs

- Marketing Expenses

- Travel & Accommodation

This makes future reporting significantly cleaner.

Days 2–7: Build Digital Record-Keeping Systems

The first week should focus heavily on documentation discipline.

Many businesses lose critical records during this stage simply because there is no organized storage process.

Create a Central Audit Repository

Every company should maintain a secure digital repository for:

- Invoices

- Contracts

- Bank statements

- Government certificates

- Tax filings

- Vendor agreements

- Employee records

The filing structure should be standardized from the start.

For example:

- Finance > Bank Statements > 2026

- HR > Employee Contracts

- Tax > VAT Filings

- Legal > MoA & AoA

Consistency matters more than complexity.

Capture All Early Expenses Immediately

One of the most common startup mistakes is delaying expense collection.

Founders often assume they can “organize receipts later.”

That rarely happens successfully.

Track immediately:

- Company formation costs

- Legal fees

- Translation charges

- Software purchases

- Visa expenses

- Travel costs

- Initial deposits

Every expense should have supporting evidence.

Days 8–14: Complete Authority Registrations

Once the operational structure is stable, focus shifts to regulatory registrations.

This stage is critical for maintaining compliance inside Saudi Arabia.

Register with ZATCA

Zakat, Tax and Customs Authority registration is one of the most important early compliance steps.

Depending on the company structure, this may involve:

- Corporate Income Tax

- Zakat registration

- VAT registration

- E-invoicing preparation

Many businesses incorrectly delay this process until revenue begins.

That can create unnecessary penalties and compliance exposure.

Open the Corporate Bank Account

The corporate bank account should become the central payment channel immediately.

Avoid operating through personal founder accounts once the business entity exists.

This creates accounting confusion and weak audit trails.

Banks may also request:

- Commercial Registration

- Articles of Association

- National Address

- Board resolutions

- UBO documentation

- Tax certificates

Prepare these early to avoid delays.

Align HR Systems with GOSI and MHRSD

Payroll compliance should begin before hiring activity accelerates.

Key registrations include:

- General Organization for Social Insurance (GOSI)

- Ministry of Human Resources and Social Development (MHRSD)

These systems govern:

- Social insurance

- Saudization compliance

- Employment records

- Workforce regulations

Poor alignment between HR and finance creates immediate compliance risk.

Days 25–30: Execute the First Monthly Close

Do not wait until year-end to “see how finances look.”

Your first month-end close should happen immediately.

Even if transactions are minimal.

Reconcile Bank Statements

The finance team should verify:

- Every bank transaction

- Expense classifications

- Outstanding balances

- Founder reimbursements

- Vendor payments

This creates financial discipline early.

Review the Trial Balance

The trial balance helps identify:

- Duplicate postings

- Missing entries

- Incorrect classifications

- Unusual balances

Fixing errors monthly is significantly easier than fixing them annually.

Generate Early Management Reports

Even simple reporting matters.

Monthly reports help founders monitor:

- Cash position

- Operating expenses

- Burn rate

- Vendor obligations

- Tax exposure

Strong visibility leads to better decisions.

Common Mistakes in Early Finance Setup

Mixing Founder and Company Money

This is one of the most common startup issues.

When founders pay for company expenses personally without formal reimbursement processes, audit clarity disappears.

Every transaction should be documented properly.

Delaying Documentation Collection

Receipts disappear quickly.

Waiting months to gather invoices creates major gaps in audit evidence.

Capture documentation immediately while transactions are still fresh.

Delaying ZATCA Registration

Some businesses incorrectly assume they only need registration after reaching revenue thresholds.

In practice, delayed registration often creates unnecessary complications later.

Informal Approvals Through WhatsApp

Approving major purchases verbally or through scattered chat messages creates weak internal controls.

Important approvals should be centralized and documented properly.

Delay Factors That Trigger Audit Problems

Missing Audit Trails

A clean audit trail connects:

- Invoice

- Approval

- Bank payment

- Accounting entry

Missing links create compliance risks very quickly.

Poor Cross-Department Coordination

Sometimes HR hires employees before finance completes payroll controls or GOSI onboarding.

This creates immediate regulatory exposure.

Finance, HR, and operations must move together.

The “We’ll Implement a System Later” Mentality

Many startups rely entirely on spreadsheets for too long.

Eventually, migrating messy financial data into accounting software becomes extremely expensive and time-consuming.

Even small businesses benefit from structured accounting systems early.

Practical Solutions to Improve Audit Readiness

Enforce the “No Evidence, No Payment” Rule

Train the team from the beginning:

No invoice, no approval, no payment.

This single rule dramatically improves financial discipline.

Implement a Hard Monthly Close

Treat every month-end like a mini-audit.

Lock the books by the 5th of the following month whenever possible.

This prevents retroactive changes and improves reporting accuracy.

Standardize Naming Conventions

Auditors should not struggle to locate documents.

Create consistent naming structures such as:

- VendorName_InvoiceNumber_Date

- BankStatement_March2026

- EmployeeContract_Name

Simple systems reduce operational chaos.

Key Compliance Entities Every New KSA Company Should Understand

| Entity | Why It Matters |

| Zakat, Tax and Customs Authority | Handles Corporate Income Tax, Zakat, VAT, and e-invoicing compliance |

| Ministry of Commerce | Maintains Commercial Registration records and corporate updates |

| General Organization for Social Insurance | Governs social insurance and payroll contributions |

| Ministry of Human Resources and Social Development | Manages labor compliance and Saudization |

| Saudi Business Center | Supports post-incorporation services and compliance workflows |

The Day-One Audit Evidence Checklist

Before closing your first month of operations, confirm you have secured:

- Signed Articles of Association (AoA) / Memorandum of Association (MoA)

- Corporate bank account documentation

- Proof of capital injections

- Formation expense invoices and receipts

- Vendor contracts and agreements

- Approval matrix documentation

- ZATCA registration certificates

- Employee contracts and GOSI records

- Bank reconciliations

- Initial accounting reports

Frequently Asked Questions

Common questions from founders setting up financial governance and compliance operations in Saudi Arabia.

-

A day-one compliance plan for a new Saudi company covers every foundational layer your financial and operational infrastructure needs before the first transaction is recorded or the first employee is onboarded. At minimum, it includes:

- Accounting policies — defining revenue recognition, expense categorization, and the accrual basis adopted under SOCPA standards

- Chart of accounts setup — structuring your ledger to cleanly separate founder equity, operational expenditure, cost of goods sold, and payroll

- Approval workflows — establishing tiered, role-based digital sign-off processes for all expenses and vendor payments before any funds leave the business

- Audit documentation standards — defining how every transaction is vouched, stored, and retrievable for ZATCA audits or investor due diligence

- ZATCA registration — activating your tax profile and confirming Phase 2 Fatoora e-invoicing integration is live before your first invoice is issued

- Payroll compliance setup — configuring GOSI contributions, end-of-service benefit calculations, and WPS-linked salary processing

- Monthly close procedures — establishing the 5-day close discipline that keeps your trial balance reconciled and your ledger audit-ready every month

-

Yes — and from the very first month of operation, not after the first year. A monthly close creates financial discipline early and prevents the year-end accounting chaos that typically results from deferred reconciliation. When every month ends with a locked, reconciled ledger, your management accounts are always current, your bank statements always tie back to your trial balance, and your ZATCA VAT returns are based on clean, verified data. It also means that when an investor requests 12 months of management accounts, you have 12 clean, consistent months ready — not a reconstruction exercise. The cost of skipping a monthly close compounds over time: catching 12 months of errors at year-end is significantly more expensive than catching one month’s errors at a time.

-

Founders remain ultimately responsible for financial governance — that accountability cannot be fully delegated. However, operational ownership should move to qualified leadership as quickly as the company’s size and complexity justify. Depending on your stage, that means:

- A qualified Finance Manager — for companies with regular payroll, active vendor relationships, and monthly VAT filing obligations

- An outsourced or fractional CFO — for seed-stage startups where a full-time CFO hire isn’t yet justified but cross-border compliance (MISA, ZATCA, SOCPA) requires specialist oversight

- A governance advisory partner — for foreign-owned entities where the interplay between KSA statutory requirements and the parent company’s reporting standards creates complexity that needs an experienced hand

-

The most frequently identified audit readiness issues — whether discovered during a ZATCA review, a statutory audit by a SOCPA-certified auditor, or investor due diligence — fall into five categories:

- Missing invoices — vendor payments or expense entries with no supporting tax invoice or receipt attached to the transaction, making deductions unverifiable

- Poor bank reconciliations — monthly ledger balances that don’t trace cleanly back to physical bank statements, signalling a breakdown in internal controls

- Informal approvals — expenses approved via WhatsApp message or verbal sign-off with no digital audit trail, leaving no evidence of who authorized what and when

- Weak expense tracking — transactions pooled into generic categories without proper classification, making it impossible to verify tax deductibility or cost allocation

- Delayed tax registrations — ZATCA registration completed weeks or months after the company started trading, creating a period of non-compliant invoices that need to be corrected retroactively

Conclusion

Audit readiness is not something businesses prepare for once a year.

It is a daily operational habit.

The companies that scale smoothly in Saudi Arabia are usually the ones that establish clean finance governance from the beginning.

Strong controls protect:

- Founders

- Investors

- Employees

- Operations

- Reputation

Most importantly, they prevent expensive cleanup projects later.

Do not wait for revenue growth to justify proper governance.

Build the structure now.

Your future finance team, auditors, investors, and regulators will thank you for it.

Written by Syneffo solutions

At Syneffo solutions, we help newly incorporated businesses in Saudi Arabia transition from basic legal setup to fully operational, audit-ready enterprises.

From finance governance and internal controls to ZATCA readiness and operational compliance, our team supports companies building scalable and compliant foundations for long-term growth in the Kingdom.