Saudi Arabia’s venture capital and private equity ecosystem has grown significantly under Vision 2030, and for founders, that means institutional capital is genuinely accessible in a way it wasn’t a few years ago. Family offices, sovereign-backed funds, and regional VCs are actively looking to deploy into Saudi-incorporated startups.

But capital availability does not equal capital access. The founders who actually close investment rounds are the ones whose financial house is already in order when the term sheet conversation begins — not the ones scrambling to clean up their books after a VC requests a data room.

Here’s the pattern that kills deals: a founder builds a promising business, attracts investor interest, and then loses the deal during due diligence — not because the business model is flawed, but because the accounting is chaotic. A mixed chart of accounts, founder expenses sitting in the company ledger, unreconciled monthly statements, or invoices that don’t meet ZATCA compliance standards. Each of these sends the same signal to an institutional investor: weak internal controls.

Fixing this before you launch — rather than after an investor finds it — is what “investor-ready” actually means in the Saudi context. This guide walks through exactly how to build that foundation from day one.

About This Guide: This framework was developed by Syneffo Solutions‘ corporate operations and financial engineering team, drawing on direct experience building compliant, audit-ready accounting foundations for foreign-owned and locally incorporated startups across Saudi Arabia, UAE, and Malaysia.

What Does It Mean to Launch “Investor-Ready” in Saudi Arabia?

To launch investor-ready in KSA, a company must establish a localized, accrual-based accounting system that integrates with ZATCA’s e-invoicing framework from day one. This requires an audit-ready chart of accounts compliant with SOCPA standards, disciplined monthly close protocols, a clear compliance calendar for recurring tax filings, and institutional-grade monthly management accounts capable of withstanding investor due diligence.

From Bookkeeping to Financial Governance: Why the Distinction Matters

Most early-stage founders think of accounting as something that happens in the background — a bookkeeper processes expenses, a spreadsheet tracks invoices, and a tax return gets filed once a year. That mental model works fine if you’re running a lifestyle business with no plans to raise capital.

It doesn’t work in Saudi Arabia’s investment ecosystem, and it doesn’t work under ZATCA’s compliance framework.

The Saudi regulatory environment expects limited liability companies to maintain records that can withstand a formal statutory audit by a SOCPA-certified auditor. SOCPA — the Saudi Organization for Certified Public Accountants — sets the accounting standards that govern how financial records are kept, how revenues are recognized, and how audits are conducted in the Kingdom. Failing to meet these standards isn’t just an investor-relations problem. It’s a compliance problem.

And institutional investors in the region have become sophisticated enough to know the difference between a startup with clean books and one that’s been cleaned up for the pitch. Due diligence teams look at the historical consistency of financial records, not just their current state.

Cash vs. Accrual Accounting: Which One Applies to You

This question comes up early with almost every startup, and the answer is always the same: if you’re planning to raise institutional capital, you need accrual accounting from day one.

Cash accounting is simple — you record transactions when money moves in or out. But it gives you an incomplete picture. It doesn’t show what you’ve earned but haven’t received. It doesn’t show what you owe but haven’t paid. It doesn’t allow a VC to model your burn rate accurately, understand your revenue recognition policies, or assess your true working capital position.

Accrual accounting matches revenues and expenses to the period they actually occurred. That’s the standard institutional investors use to evaluate financial health, and it’s the standard SOCPA compliance expects for corporate entities.

Setting up accrual accounting from the start takes a little more structure. But retrofitting accrual accounting onto two years of cash-basis records — under a due diligence deadline — is one of the most expensive and disruptive things a startup can go through.

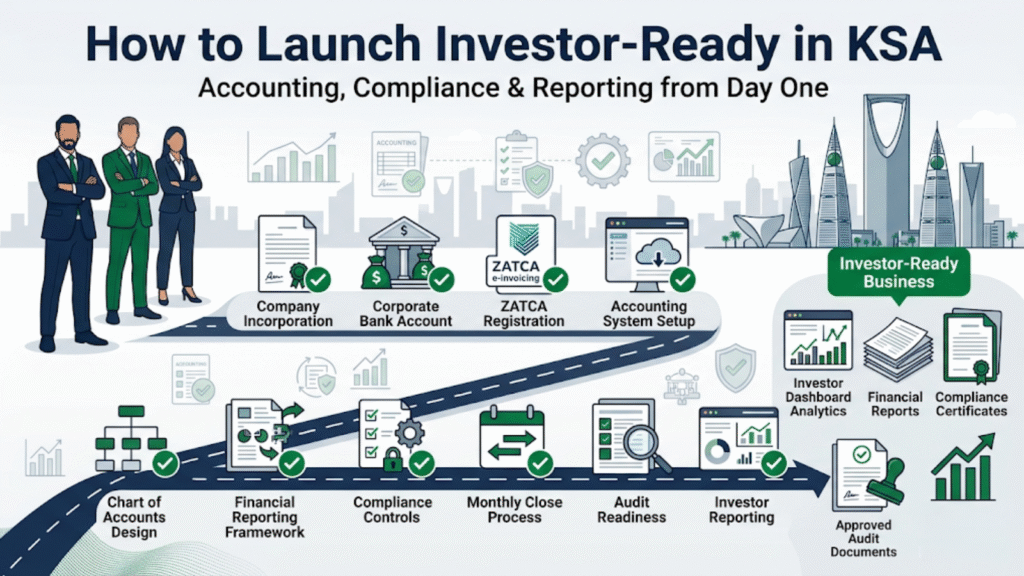

The 4-Step Blueprint for a Finance-Ready KSA Setup

The sequence matters. Founders who try to build financial governance after six months of operation spend more time unwinding bad structures than building good ones. Here’s the order that works.

Step 1: Select a ZATCA-Compliant Finance Stack

Before you issue a single invoice or record a single transaction, your accounting software needs to be in place and correctly configured.

In Saudi Arabia, this means your platform must integrate natively with ZATCA’s Phase 2 e-invoicing system — known as Fatoora. Under Phase 2, every B2B invoice must carry a cryptographic stamp, be transmitted to ZATCA’s platform in real time, and create an unalterable audit trail in your general ledger. An invoice issued without these elements is not a compliant tax invoice in Saudi Arabia.

The practical implication: global accounting tools without built-in ZATCA Phase 2 integration require custom API development to become compliant. That’s a cost and a complication you don’t need at launch. Choose a platform that has already solved this.

Your finance stack also needs to handle multi-currency transactions cleanly, support localized payroll fields, and generate the specific reporting formats that ZATCA and SOCPA require. Getting this right in week one is dramatically simpler than migrating your chart of accounts and transaction history from a non-compliant platform six months later.

Step 2: Build a Clean, Structured Chart of Accounts

A chart of accounts is the backbone of your entire financial system — the taxonomy that determines how every transaction is classified. A poorly structured one creates exactly the kind of ambiguity that derails due diligence.

The most common mistake is using a generic, out-of-the-box chart of accounts template without adapting it to the Saudi regulatory environment. When everything gets lumped into a catch-all “expenses” category, it becomes impossible to trace the origin of transactions, verify tax deductibility, or run a meaningful cost analysis.

At minimum, your chart of accounts needs clean separation between founder equity records and company operations, initial capital injections and operating revenue, operational expenditure (OpEx) and cost of goods sold (CoGS), and local payroll versus contractor payments. Each of these distinctions carries different tax and compliance implications in KSA.

Building this structure before you start recording transactions means every entry goes into the right place from the beginning. Building it after means a retroactive reclassification exercise that’s time-consuming, error-prone, and exactly the kind of thing that makes auditors — and investors — nervous.

Step 3: Commit to a Monthly Close Protocol

One of the clearest signals of financial maturity that institutional investors look for is whether a company runs a consistent monthly close process. Not a quarterly reconciliation. Not an annual catch-up. A monthly close, completed by the 5th business day of every following month, without exception.

A proper monthly close in practice means: matching your trial balance against corporate bank statements and resolving every discrepancy before locking the books; updating your cap table to reflect any bridge notes, convertible instruments, or equity movements; verifying and recording all accrued liabilities — services rendered but not yet invoiced, subscriptions that span month boundaries, payroll accruals; and locking the ledger so no backdated entries can be made.

This discipline does two things. First, it gives you a real-time picture of your financial position at the start of every month, which makes operational decisions better. Second, it means that when an investor asks for 12 months of management accounts, you have 12 clean, consistent, reconciled months ready — not a reconstruction exercise under time pressure.

Step 4: Produce Institutional-Grade Monthly Reporting

The output of your monthly close should be a standardized board pack — the financial package that institutional investors and board members use to evaluate performance.

A proper board pack contains three core financial statements: your Balance Sheet, Income Statement, and Cash Flow Statement. These are the minimum. Beyond the three core financials, the board pack should include an operational KPI dashboard covering monthly burn rate, cash runway in months, customer acquisition cost, revenue per employee, and whatever unit economics are most relevant to your business model.

Producing this consistently from month one — even before you have investors — establishes the baseline that makes all future investor conversations easier. When a VC asks “can you share the last six months of management accounts?”, your answer should be a data room link, not a preparation exercise.

Financial Mistakes That Derail Investment Rounds

Understanding what kills deals matters just as much as understanding what builds readiness.

Commingling Founder and Corporate Funds

Early in the company’s life, when there’s no clean banking infrastructure yet, founders sometimes pay for setup costs, subscriptions, or office supplies from personal accounts — intending to reimburse themselves later. The problem is that without proper voucher records and clear expense claims, these transactions create ambiguity in the capitalization records. Was it a founder loan? A capital injection? A personal expense that should be written off?

When a due diligence team finds unvouched transactions in the early months, they extend the investigation to every subsequent period. The fix is establishing the corporate bank account and expense policy before you incur any operational costs, and documenting every early expense with an official receipt or invoice attached directly to the transaction record.

Treating E-Invoicing as a Post-Revenue Problem

“We’ll sort out ZATCA compliance once we start billing clients” is one of the most expensive delays a Saudi startup can make. By the time you’re issuing your first invoice to a corporate client, your Fatoora integration should already be tested and operational. Retroactively correcting non-compliant invoices issued to VAT-registered Saudi businesses creates a compliance liability that you don’t want sitting on your books when a ZATCA auditor arrives.

Ignoring the Compliance Calendar

Regulatory deadlines don’t care about your product roadmap. VAT filing deadlines, corporate income tax submissions, GOSI payroll cycles, and municipal license renewals all operate on their own schedules. Missing any of them attracts statutory penalties that show up as unexpected liabilities in your financial statements — exactly the kind of thing that raises red flags during due diligence.

What Breaks Down During Due Diligence

Beyond early-stage mistakes, there are specific structural problems that consistently stop investment deals from closing once the data room opens.

Unreconciled balance sheets. If your historical monthly reports don’t trace cleanly back to corporate bank statements, a financial analyst will assume internal controls are broken — because they are. Reconciliation isn’t just an accounting exercise. It’s the evidence that your financial data is reliable.

Unvouched vendor payments. Large payments for marketing, software development, or professional services without matching compliant ZATCA tax invoices from those vendors create a tax audit risk. Unsubstantiated deductions can be disqualified, creating a retroactive tax liability that shows up as a hidden problem on your cap table.

Missing labor compliance records. If your startup has been paying staff without registering them through the Wages Protection System (WPS) or without maintaining active GOSI records, you’ve created a historical labor liability. Investors in the Saudi market know to look for this specifically, and finding it mid-round is a serious red flag.

Practical Steps to Build Your Compliance Defense

Enforce a Two-Tier Expense Approval Workflow

No corporate funds should leave the business without a matching official invoice or digital receipt attached directly to the transaction in your ledger. Two-tier approval — one person requests, a second person authorizes — prevents both errors and the ambiguity that creates problems during audit.

Build a Regulatory Dependency Matrix

Create a shared compliance calendar with named internal owners for every recurring statutory filing. VAT returns, corporate income tax submissions, GOSI payroll cycles, ZATCA reporting windows, municipal license renewals, MISA quarterly investment reports for foreign-owned entities. Each deadline needs an owner, a reminder, and a consequence attached to it.

Consider Fractional Finance Leadership

If a full-time CFO isn’t in your seed-stage budget, a fractional or virtual CFO who understands the specific cross-border compliance interactions between MISA, ZATCA, and SOCPA will pay for themselves many times over. They ensure your financial architecture is set up correctly from the start — and give institutional investors confidence that someone with appropriate expertise is watching the numbers.

KSA’s Key Financial Regulatory Bodies

| Authority / Framework | Structural Requirement | Operational Focus |

| ZATCA (zatca.gov.sa) | VAT returns, corporate income tax, Fatoora e-invoicing | Tax compliance and transaction integrity |

| SOCPA | Saudi accounting standards and audit credentials | Chart of accounts, revenue recognition, audit readiness |

| GOSI (gosi.gov.sa) | Employee payroll and social insurance records | WPS compliance and payroll audit readiness |

| Ministry of Commerce (MOC) (mc.gov.sa) | Statutory filings and corporate governance | Annual financial statements via Qawaem portal |

| MISA (misa.gov.sa) | Foreign investment compliance reporting | Quarterly reports for foreign-owned entities |

The Day-One Investor-Ready Checklist

Use this before you open for business — and revisit it monthly until every item is consistently green.

- [ ] Accounting standard: Is your ledger configured for IFRS/SOCPA accrual accounting rather than cash-basis?

- [ ] ZATCA integration: Is your invoicing software integrated with ZATCA Phase 2 Fatoora and tested before your first invoice?

- [ ] Clean capital records: Are all founder loans and seed investments backed by signed agreements matching actual bank deposit records?

- [ ] Monthly close mandate: Is there a defined process to lock the general ledger by the 5th business day of every following month?

- [ ] Clean audit trail: Does every asset purchase and service expenditure link directly to an uploadable voucher or vendor receipt?

- [ ] WPS compliance: Is your corporate bank account connected to a compliant salary processing system through the Wages Protection Program?

- [ ] National Address on invoices: Is your verified SPL commercial address correctly displayed on all outbound invoice layouts?

- [ ] Compliance calendar: Are all recurring statutory deadlines entered in a shared system with named internal owners?

- [ ] Expense policy: Is a two-tier expense approval workflow documented and enforced before any operational spending begins?

Frequently Asked Questions

Common questions from founders building investor-ready financial operations in Saudi Arabia.

-

If you’re planning to raise institutional capital, accrual accounting is non-negotiable from day one. Cash accounting fails to show outstanding liabilities, recurring commitments, or recognized revenue pipelines — giving investors an incomplete picture of the business. Accrual accounting is also the standard required for SOCPA compliance and matches the due diligence frameworks used by institutional investors across the region. Retrofitting accrual accounting onto two years of cash-basis records under a due diligence deadline is one of the most disruptive and expensive exercises a startup can go through.

-

At minimum, a standardized board pack containing a Balance Sheet, Income Statement, and Cash Flow Statement, produced by the 5th business day of every month. Beyond the three core financials, include an updated capitalization (cap) table reflecting any changes in equity or debt structure, and an operational KPI dashboard covering monthly burn rate, cash runway in months, customer acquisition cost, and the unit economics most relevant to your model. Consistency matters more than format — investors want to see 12 months of the same report structure, not 12 different formats.

-

Yes. Under Saudi corporate law, LLCs are required to submit audited financial statements annually through the Ministry of Commerce’s Qawaem portal. This is a legal requirement, not an optional best practice. Setting up audit-ready workflows from day one — clean ledgers, proper vouching, consistent monthly closes — means your year-end audit is a straightforward, predictable process rather than an expensive and stressful reconstruction exercise that disrupts your entire operations team.

-

Mandatory VAT registration is required when your taxable supplies exceed 375,000 SAR over any 12-month period. However, startups can opt for voluntary registration if taxable turnover or purchases exceed 187,500 SAR — which is worth considering for early-stage companies with significant setup costs, since VAT registration allows you to reclaim input VAT paid on those expenses. For most investor-backed startups with meaningful early spending on infrastructure, technology, and office setup, voluntary early registration is the right decision.

-

The non-negotiable requirement is native ZATCA Phase 2 Fatoora integration — not a workaround or a custom API build. Beyond that, the platform needs to support multi-currency transactions, generate localized payroll reports, and produce the chart of accounts structures that SOCPA compliance requires. Evaluate any platform against these specific Saudi requirements before committing — not after you’ve migrated your transaction history onto it. The cost of switching platforms mid-operation, including data migration and re-configuration, significantly outweighs the cost of choosing correctly at the start.

Conclusion: Financial Discipline Drives Valuation

There’s a direct relationship between the integrity of a startup’s financial data and the confidence investors bring to a valuation conversation. Clean, consistent, audit-ready books don’t just prevent problems during due diligence — they actively support a higher valuation because they reduce perceived execution risk.

Rushing into the Saudi market without financial governance might help you launch slightly faster. But it introduces administrative risks that sophisticated investors will identify, and it creates a cleanup exercise that costs more in time and money than building it correctly from the start.

By establishing a ZATCA-compliant accounting stack, committing to rigid monthly close protocols, enforcing internal controls from your first operational week, and producing consistent institutional-grade reporting, you protect your capitalization table and ensure your startup is always positioned to move quickly when the right capital partner arrives.

The best time to build investor-ready financial infrastructure is before you need investors. That time is now.

Want to ensure your Saudi startup’s financial foundation is investor-ready from day one? Syneffo Solutions designs automated back-office frameworks, handles complex GCC market entries, and builds ZATCA-compliant, SOCPA-ready accounting foundations for global founders.

Contact our Saudi Market Experts Today

About the Author Written by the Syneffo Solutions Compliance Team — specialists in KSA market entry, corporate structuring, and business process automation for global founders. Syneffo operates across Saudi Arabia, UAE (Sharjah), and Malaysia (Selangor) with 25+ years of combined executive experience. Contact us at info@syneffosolutions.com